Interest Income General Journal

Interest Earned Double Entry Bookkeeping

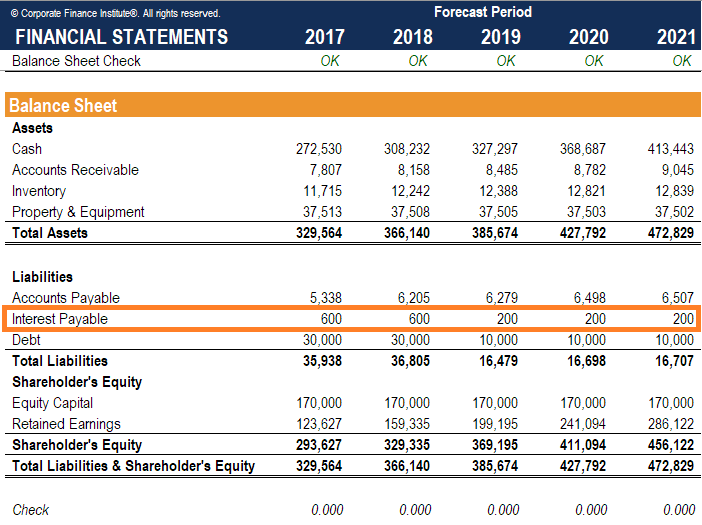

Interest Payable Guide Examples Journal Entries For Interest Payable

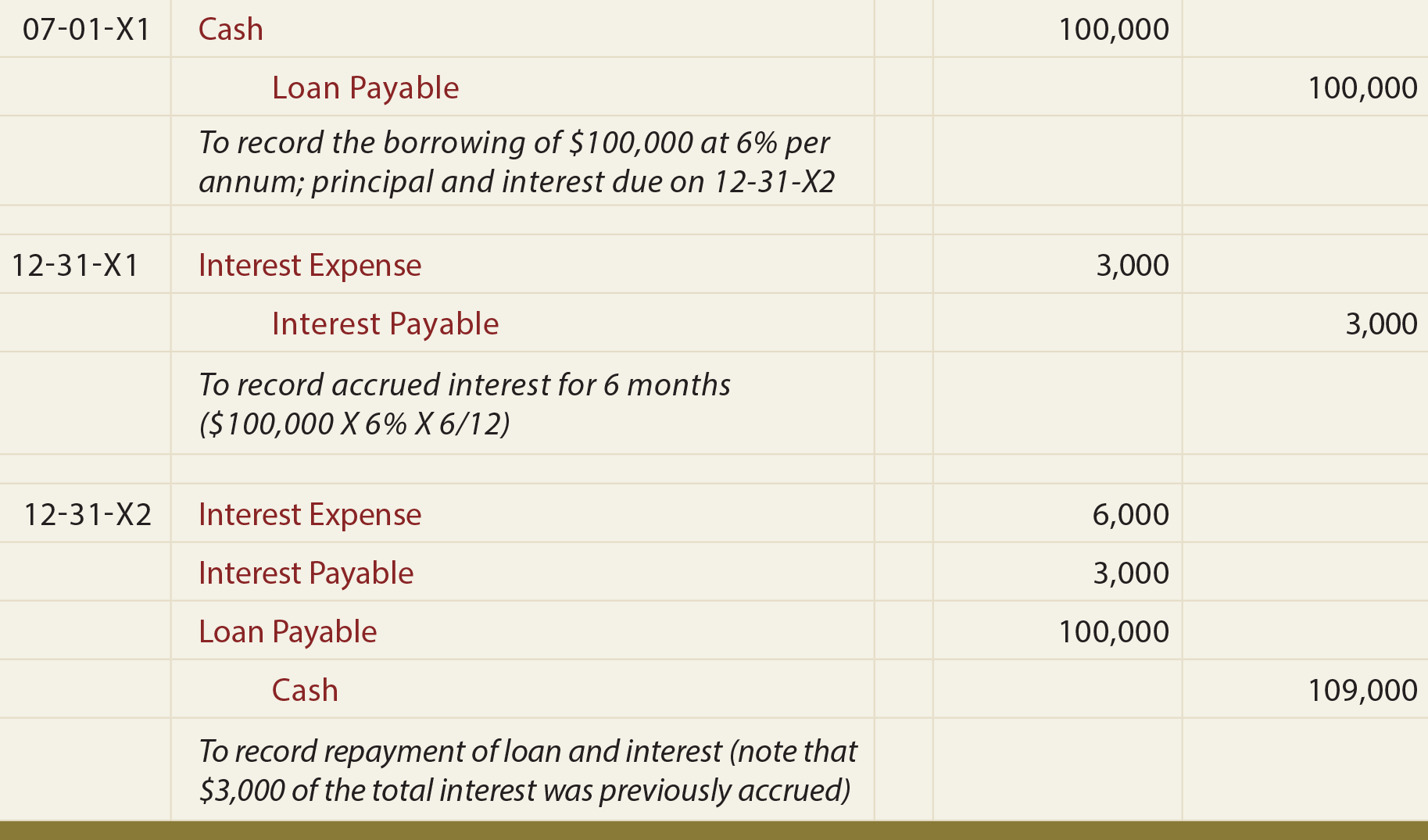

Loan Note Payable Borrow Accrued Interest And Repay Principlesofaccounting Com

Accrued Interest Definition Formula Journal Entries Play Accounting

Accrued Revenues

Unearned Revenue Journal Entry Double Entry Bookkeeping

Loan amount interest rate number of due months 12 200 000 12 3 12 6 000.

Interest income general journal. In this step all the accounting transactions are recorded in general journal in a chronological order the general journal is maintained essentially on the concept of double entry system of accounting where each transaction affects at least two accounts. Interest income is the amount of interest that has been earned during a specific time period. Interest income is the revenue earned by lending money to other entities and the term is usually found in the company s income statement to report the interest earned on the cash held in the savings account certificates of deposits or other investments. A journal entry is the first step of the accounting or book keeping process.

The amount of interest may have been paid in cash or it may have been accrued as having been earned but not yet paid. In the latter case interest income should only be recorded if receipt of the cash is probable and you can ascertain the amount of the payment to be received. Other names used for general journal are journal book. Examples of accrued income interest on investment earned but not received rent earned but not collected commission due but not received etc.

This amount can be compared to the investments balance to estimate the return on investment that a business is generating. It is computed by multiplying the principal amount by the interest rate for the period the money was lent. As the income has been earned but not received it needs to be accrued for in the month end accounts. The double entry bookkeeping journal entry to show the accrued interest income is as follows.

The interest expense is the bond payable account multiplied by the interest rate. For the year ending december 2018. Journal entry for accrued income recognizes the accounting rule of debit the increase in assets modern rules of accounting. Entry to record the disbursement of loan and interest income receivable.

Dr bond payable 9 935. Under the accrual basis of accounting a business should record interest revenue even if it has not yet been paid in cash for the interest as long as it has earned the interest. The payable is a temporary account that will be used because payments are due on january 1 of each year. This is done with an accrual journal entry.

Learn everything you need to know about interest income. Interest income is money earned by an individual or company for lending their funds either by putting them into a deposit account in a bank or by purchasing certificates of deposits callable certificate of deposit a callable certificate of deposit is an fdic insured time deposit with a bank or other financial institutions. Definition classification and presentation journal entries and examples. Interest revenue is the earnings that an entity receives from any investments it makes or on debt it owns.

Interest income refers to revenue earned for lending money. It is treated as an asset for the business. A business earns interest on its money deposits of 1 000 but does receive the amount into its bank account until after the month end. Cr interest payable 96 000.

General Journal In Accounting Definition Examples Format

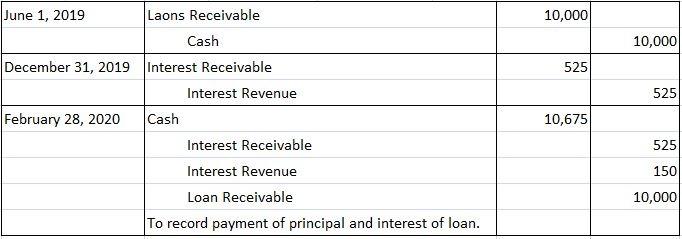

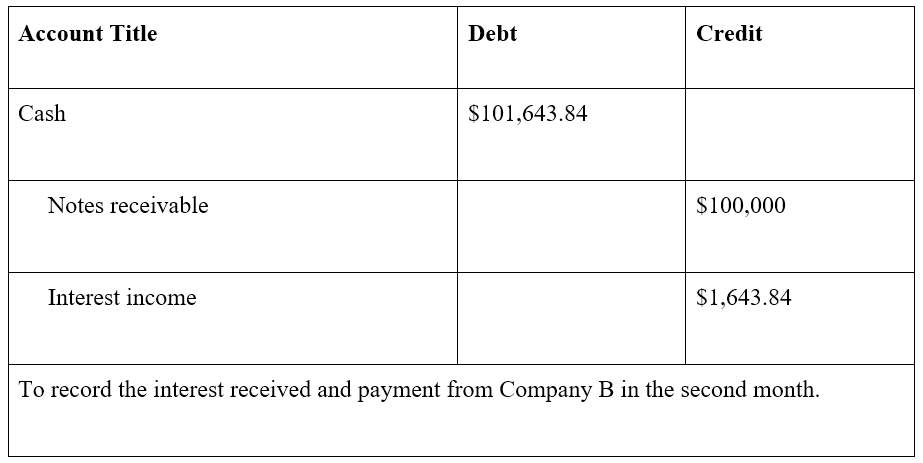

Recording Notes Receivable Transactions

Entries For Fixed Deposit Fd Fixed Deposit And Interest Entries

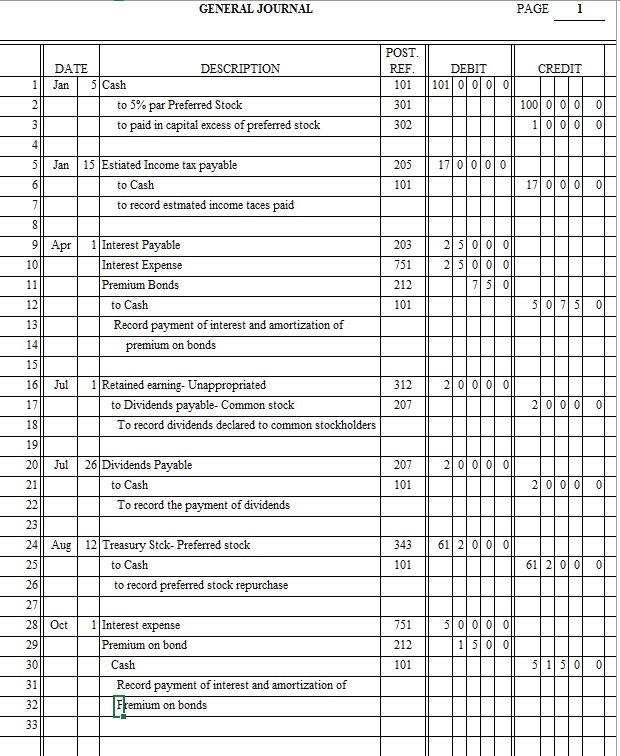

The General Journals Is Provided Below With The Ti Chegg Com

Loan Repayment Principal And Interest Double Entry Bookkeeping

Debt Securities Principlesofaccounting Com

Basics Of Accounting Chart Of Accounts General Journal General Led Chart Of Accounts Accounting Accounting Career

What Are Notes Receivable Examples And Step By Step Guide

Closing Entries Accounting Simplified

Basics Of Accounting Chart Of Accounts General Journal General Led Chart Of Accounts Accounting Cost Accounting

Closing Entries Using Income Summary Accounting In Focus

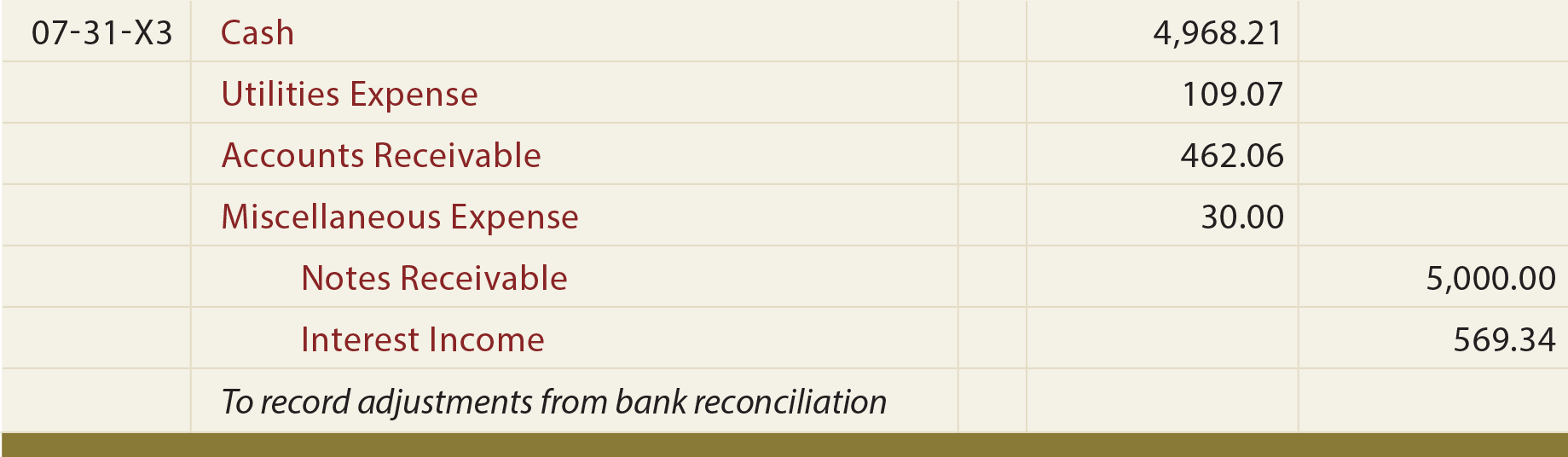

Bank Reconciliation Principlesofaccounting Com

Discounting Notes Receivable