Interest Income General Journal Entry

Interest Earned Double Entry Bookkeeping

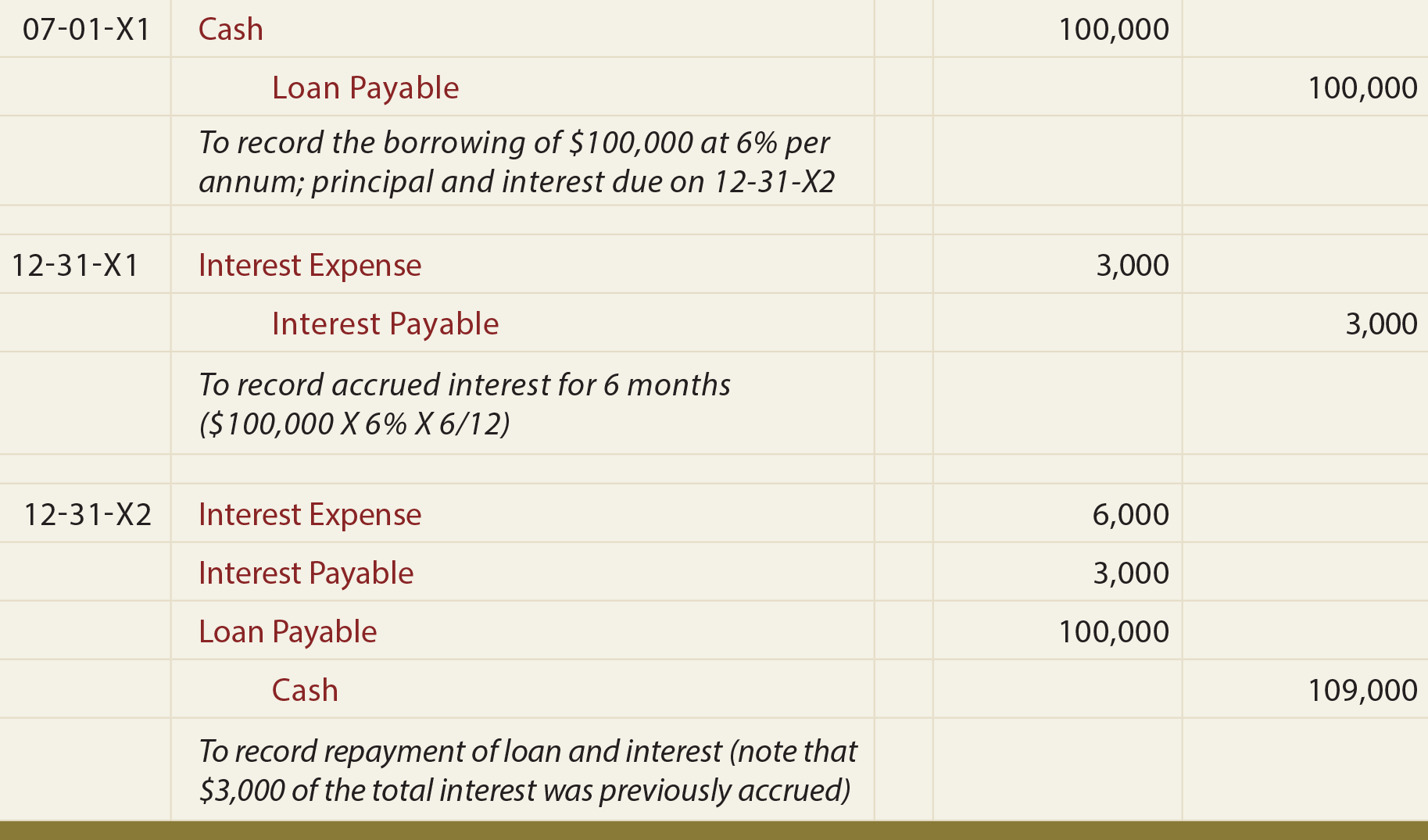

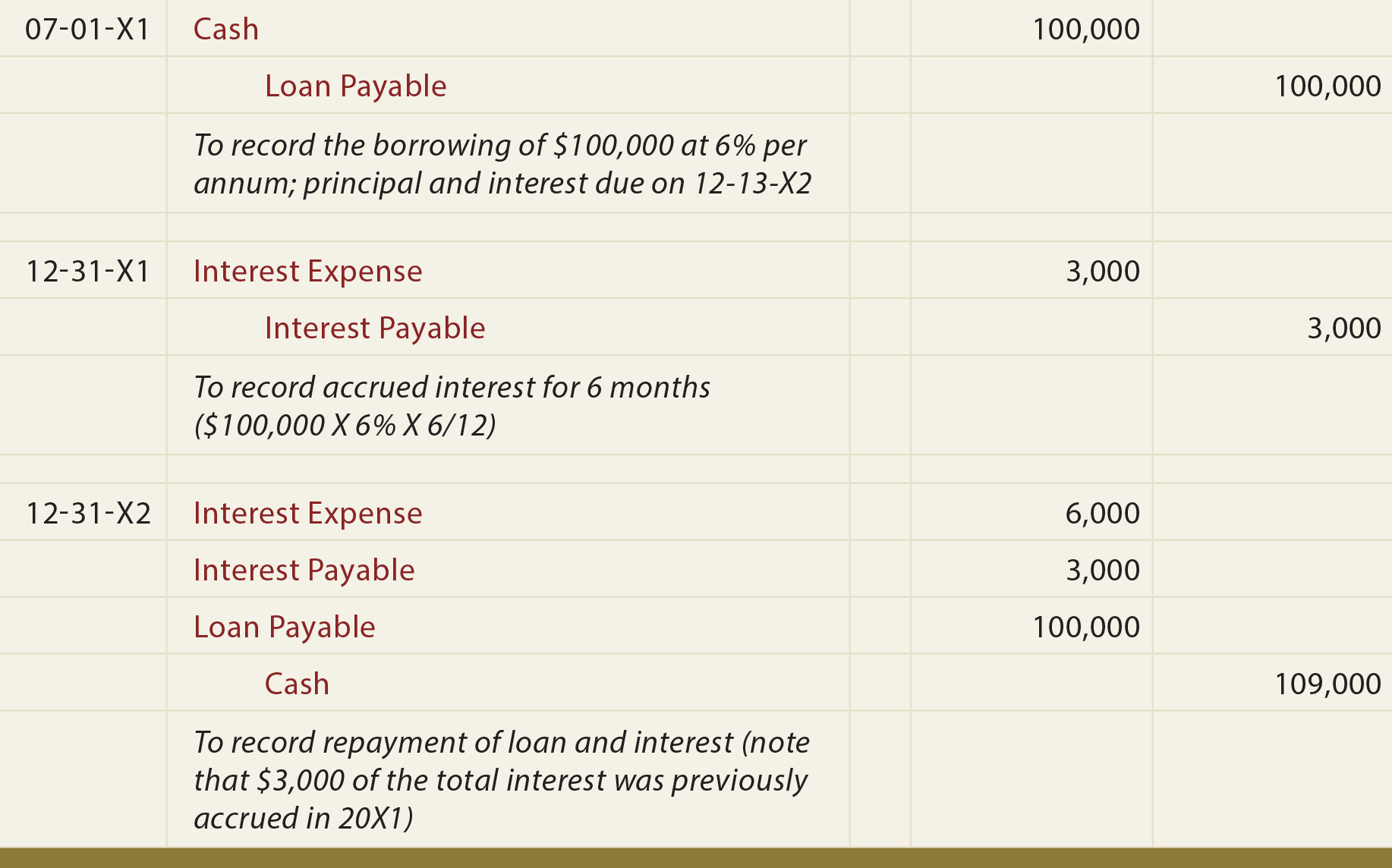

Loan Note Payable Borrow Accrued Interest And Repay Principlesofaccounting Com

Accrued Interest Definition Formula Journal Entries Play Accounting

Interest Payable Guide Examples Journal Entries For Interest Payable

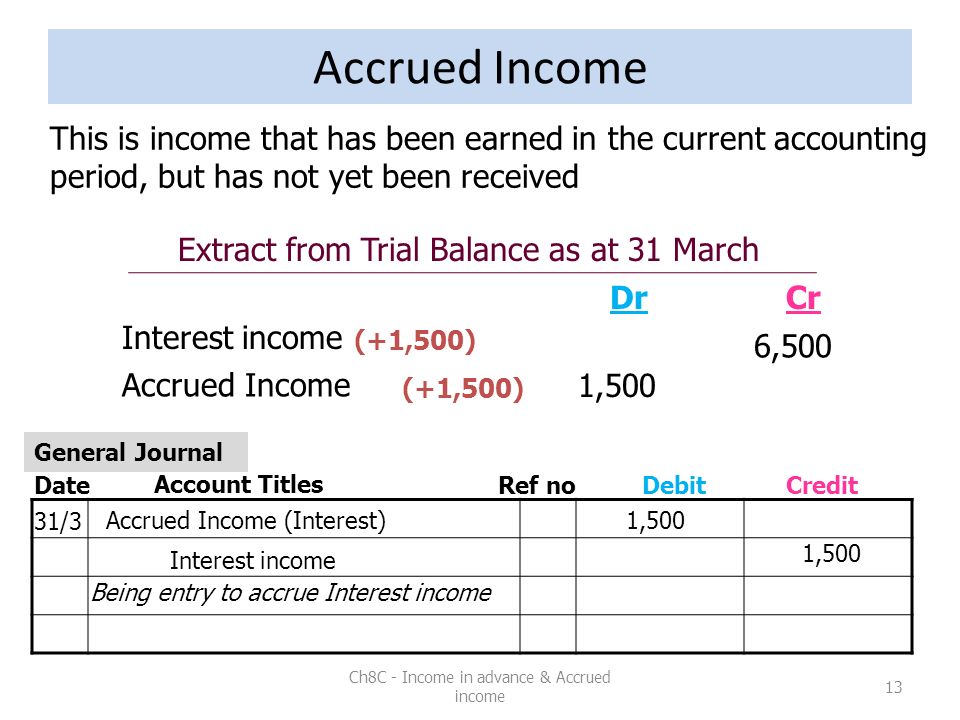

Accrued Revenues

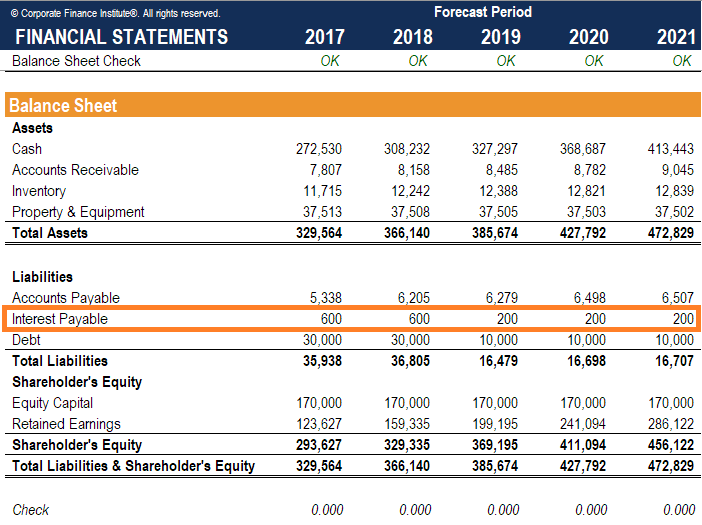

Accounting Practices 501 Chapter 8 Balance Day Adjustments Income In Advance Accrued Income Cathy Saenger Senior Lecturer Eastern Institute Of Technology Ppt Download

Interest income journal entry overview.

Interest income general journal entry. As the income has been earned but not received it needs to be accrued for in the month end accounts. Some companies prefer to mention this type of income as penalty income. If it doesn t or an accrual hasn t been posted then an adjusting entry can be posted to the general ledger. It is reported within the interest income account in the general ledger.

According to golden rules of accouting. The double entry bookkeeping journal entry to show the accrued interest income is as. Journal entry for income received in advance. Hence the company needs to account for interest income by properly making journal entry at the end of the period.

Journal entry for income received in advance recognizes the accounting rule of credit the increase in liability. Many accounting departments keep amortization tables illustrating interest expense. Compound interest is calculated using a similar method. Likewise this type of income is usually earned but not yet recorded during the accounting period.

For example if a business has deposited 10 000 with a bank earning 5 simple interest at the end of the year the interest earned is 10 000 x 5 500. This income is taxable as per irs and the ordinary tax rate is applicable for this income. Analyze the treatment of the interest received by the company and pass the necessary journal entries in the books of the bank. It is treated as an asset for the business.

Also known as unearned income it is income which is received in advance however the related benefits are yet to be provided it belongs to a future accounting period and is still to be earned. A business earns interest on its money deposits of 1 000 but does receive the amount into its bank account until after the month end. It is income earned during a particular accounting period but not received until the end of that period. So the bank will recognize its income of.

Journal entry for accrued income recognizes the accounting rule of debit the increase in assets modern rules of accounting. In the present case the employee was not able to pay the loan principal amount as well as the interest portion on the due date. The formula however calculates interest earned on interest. Interest income is a type of income that is earned and accumulated with the passage of time.

Real a c debit what comes in credit what goes out nominal a c debit all losses and expenses credit all profits and. If the interest is deposited in the bank account of the business the accounting journal to post this interest earned to the accounting records would be as follows. The interest portion got accrued in accounting year ending in 2018 but not received.

The Adjusting Process And Related Entries Principlesofaccounting Com

Chapter 13 Skyline College Ppt Download

Fixed Deposit Journal Entry Double Entry Bookkeeping

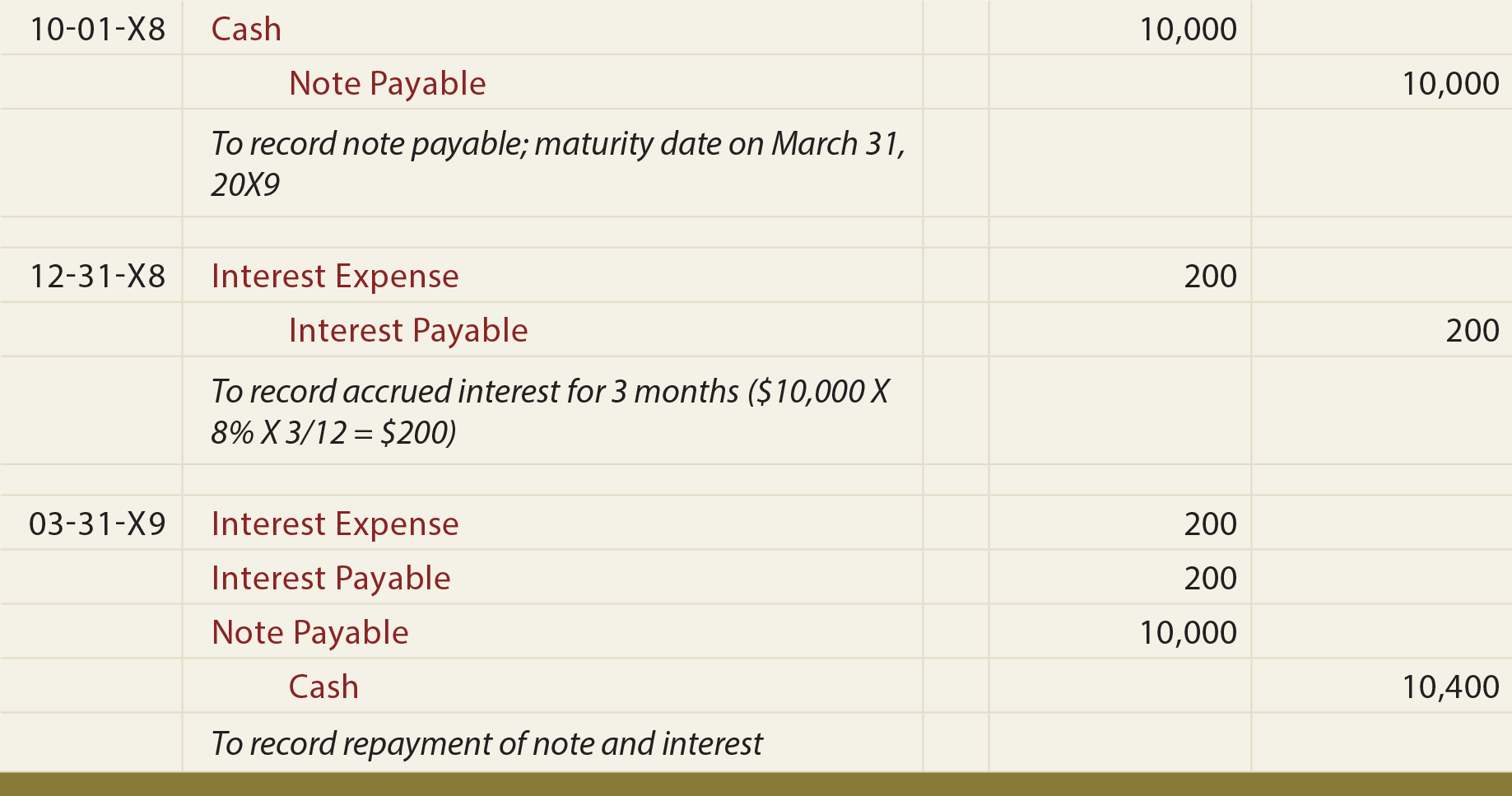

Notes Payable Principlesofaccounting Com

Loan Repayment Principal And Interest Double Entry Bookkeeping

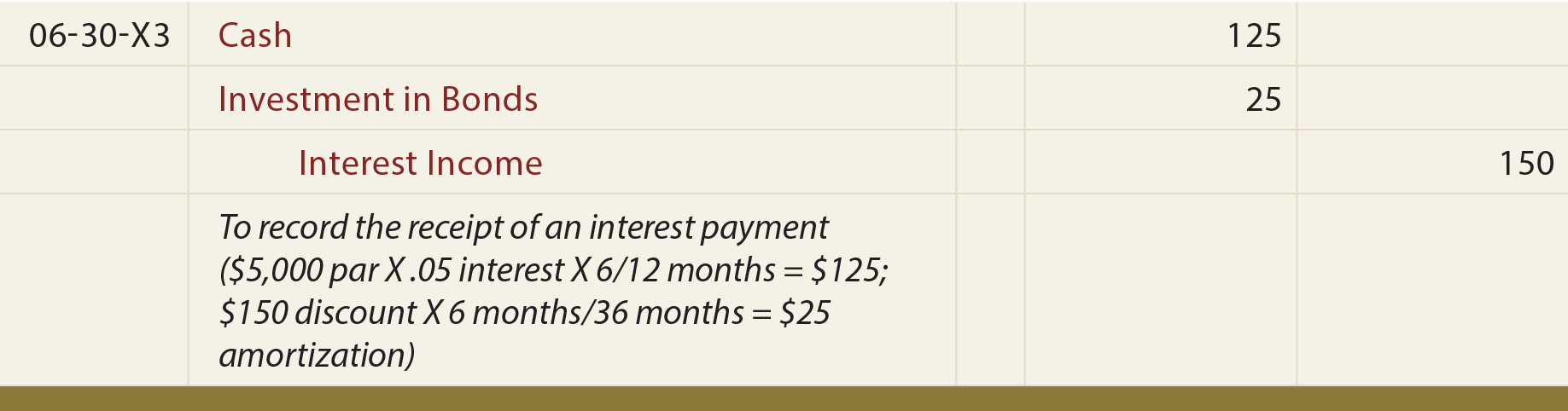

Held To Maturity Securities Principlesofaccounting Com

Entries For Fixed Deposit Fd Fixed Deposit And Interest Entries

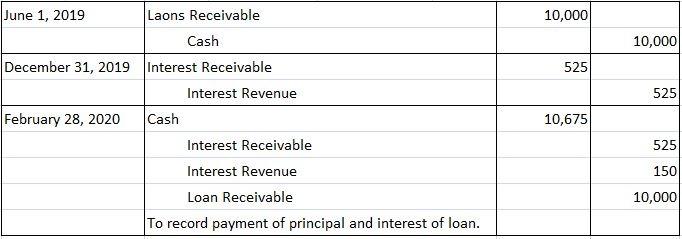

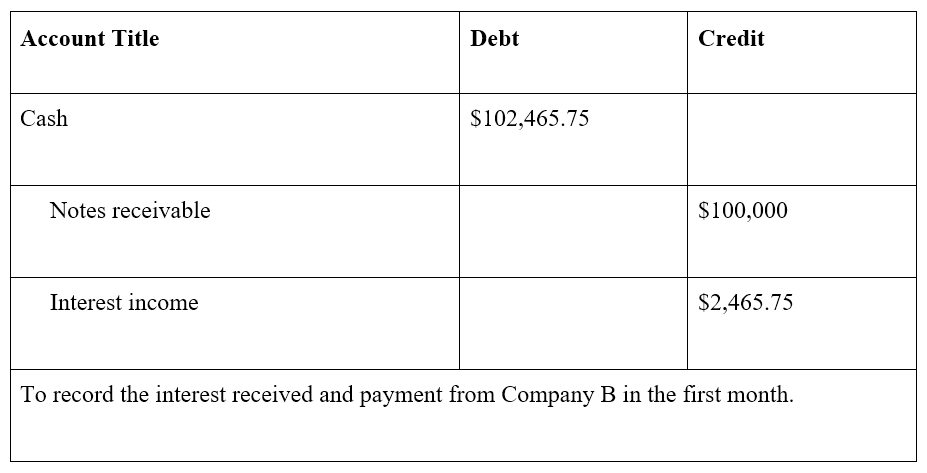

Notes Receivable Principlesofaccounting Com

Effective Interest Amortization Methods Principlesofaccounting Com

What Are Notes Receivable Examples And Step By Step Guide

Recording Notes Receivable Transactions

How To Create Journal Entries In Tally

Journal Entries Of Loan Accounting Education